I was recently invited to share my thoughts with almost 400 delegates of the 1st Virtual Youth Congress organised by the Rotary Club of Makati Jose P Rizal. It was a mutually meaningful talk based on the feedback of the very engaged attendees and at my end, it was quite inspiring to do my own share of addressing the still prevalent “sandwich generations” among Filipinos.

I call it “sandwhich generation” when children take care of their ageing parents at retirement (because they have not prepared for it financially) while they take care of their obligation to their own family…thereby affecting also their capacity to prepare for their own retirement.

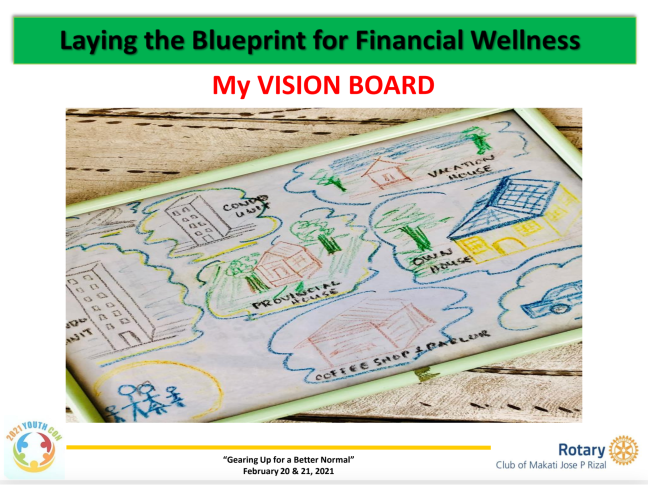

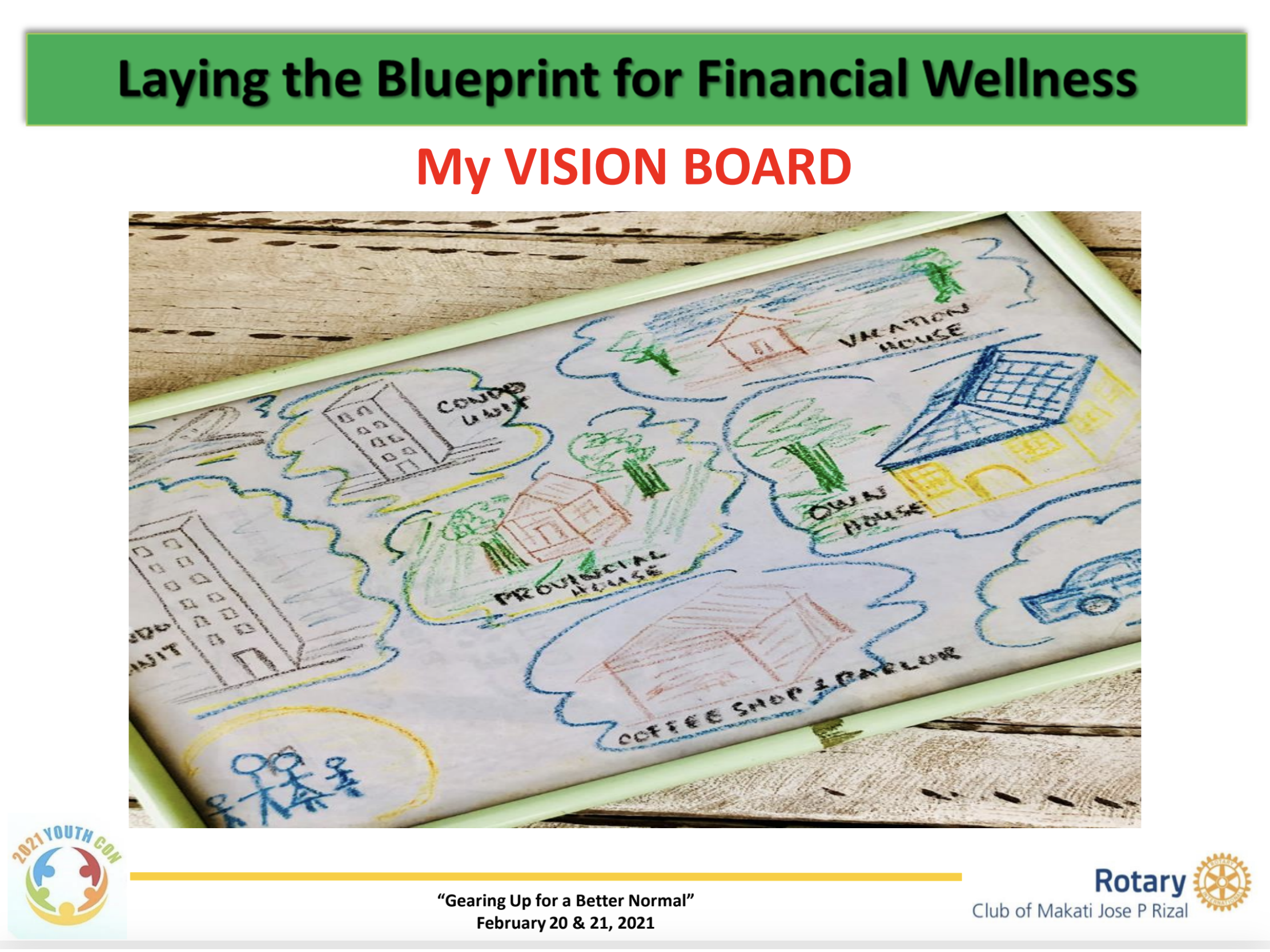

I shared with them my own vision board that I drew 22 years ago. It is a crude representation of the future that I then want but it has served as my guide and the basis for a more comprehensive financial plan that i diligently implement. I am happy to say that all except two goals (we were only blessed with one child and at my age, I can’t bear another one (sigh) and the brand of dream car that I now find impractical to buy).

My crude Vision Board reflecting the future that I want which I drew 22 years ago.

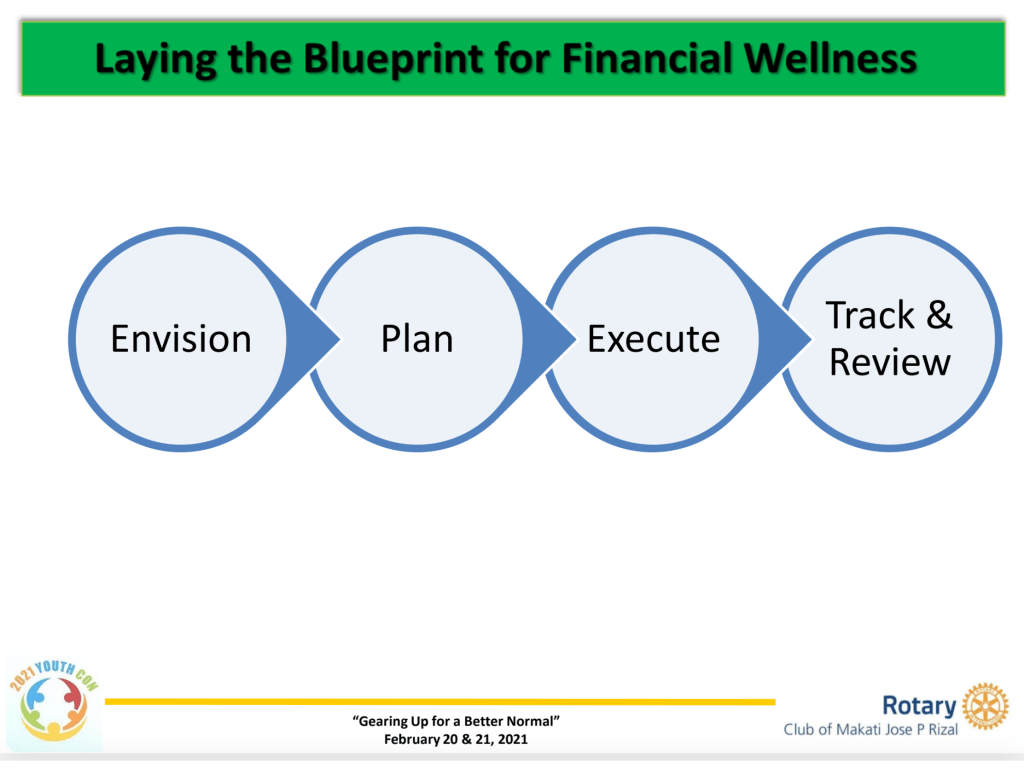

I outlined 4 steps as a guide in preparing one’s road map towards Financial Wellness:

- Envision – Know what you want in every stage in your life. Visualise how the future looks like for you. Just the broad strokes.

- Plan – Put a price tag to the future that you want. Once you know what you want, you can then determine how much fund you need to build-up between now and the time you need it. The key word is “build-up” which requires you to start early to take advantage of the time horizon where you can grow your money.

- Execute – Start putting the elements of your Financial Plan. One thing we discovered about investing is that people generally have a mismatch of their goals and the investment vehicle they use. For example, a young couple wants to start early in setting up the college education plan for their 2-year old child and yet, they put their money in a savings account with little or negligible interest income. A basic principle in investing is that you can take more risks (ie invest in an equity fund that may be more volatile) if you have a longer time horizon.

- Track and Review – Our goals and aspirations change so it is important to track and review where we are so far and make the necessary adjustments while we still have time.

I closed by reminding the delegates that their youth is their main advantage and they must not waste it by starting early and making the right choices.